FDIC vs SIPC

What is the difference between FDIC and SIPC protection? This beginner-friendly guide explains how banks and brokerage accounts are protected using simple real-world examples anyone can understand.

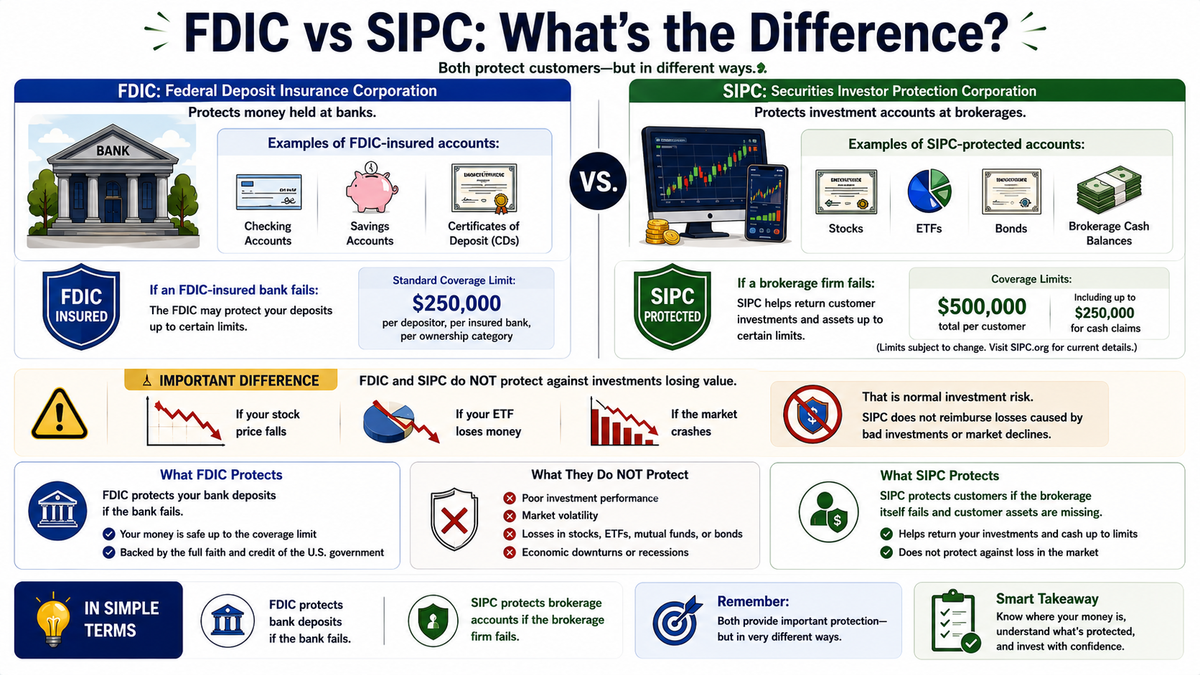

Imagine you keep money in two different places.

The first place is:

- a bank savings account

The second place is:

- an investing account holding stocks and ETFs

Both places protect customers differently.

That is where FDIC and SIPC come in.

FDIC stands for:

Federal Deposit Insurance Corporation

The FDIC protects money held at banks.

Examples include:

- checking accounts

- savings accounts

- certificates of deposit (CDs)

If an FDIC-insured bank fails:

The FDIC may protect your deposits up to certain limits.

SIPC stands for:

Securities Investor Protection Corporation

SIPC protects investment accounts at brokerages.

Examples include:

- stocks

- ETFs

- bonds

- brokerage cash balances

If a brokerage firm fails:

SIPC helps return customer investments and assets up to certain limits.

But there is a very important difference.

FDIC and SIPC do NOT protect against investments losing value.

For example:

- if your stock price falls

- if your ETF loses money

- if the market crashes

That is normal investment risk.

SIPC does not reimburse losses caused by bad investments or market declines.

Instead:

SIPC mainly protects customers if the brokerage itself fails and customer assets are missing.

Meanwhile FDIC protects bank deposits if the bank fails.

In simple terms:

FDIC protects bank deposits, while SIPC protects brokerage accounts if the financial institution fails.